Following the tradition of evaluating the current year’s investment plan at the end of November in preparation for writing the next year's plan, I just finished the review of 2023. If you have not read “The 2023 Game Plan” posted on January 1st of this year, you might want to do that before moving on.

Overall, I am pleased with the year to date results of the Stock Talk portfolio. The stocks have delivered a return of 20.9% while GIC’s/Cash did 5.3% for a total portfolio return of 13.1%. The stocks in the portfolio beat the TSX: 5.3%, Dow: 9.6%, and S&P: 20.3% while lagged the Nasdaq: 37.8%. Below are some of the learnings and drivers of the results.

Note: Each of the following points correspond to the strategies laid out in “The 2023 Game Plan”

1. Plan: Hold the stocks bought in 2022 with two swaps: Telus for Bell and Paypal for Square.

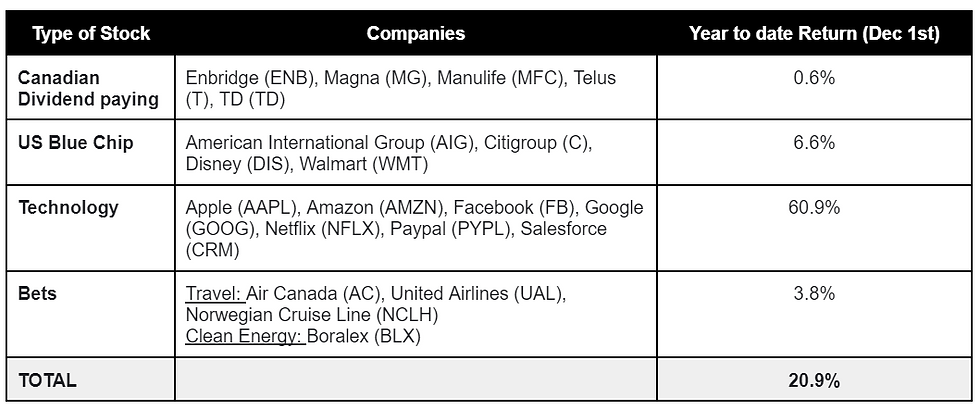

Result: The Stock Talk portfolio delivered a solid year with an overall return of 20.9% year to date. However, not all stocks performed equally, which helps reinforce some previous learnings and gather some new ones, see more below.

The value of a diversified portfolio stands the test of time. Not only across different segments but also within each segment. For instance, had all the Stock Talk portfolio been concentrated on Canadian dividend paying stocks, it would not have made any money. On the other hand, if it had been all in tech, it would have been a fantastic year. However, the same tech stocks that combined are up 60.9% in 2023 had experienced a decline of 44% in 2022. So, until we have a crystal ball, a diversified portfolio that can protect from a downturn, and still give exposure in a bull market continues to be one of the best ways to invest.

The best performing part of the Stock Talk portfolio was the technology stocks (60.9%). All stocks performed ahead of the index (Nasdaq at 37.8%) with the exception of Paypal (-22.7%). At this point last year, Paypal had already lost 76% from its peak in 2021 and seemed to be set for a recovery in 2023. Unfortunately, it didn’t happen and swapping Paypal (PYPL) at -22.7% for Block (formerly known as “Square”, SQ) at 0.6% didn’t pay off.

The worst performing part of the portfolio was the Canadian Dividend paying stocks. All stocks except Manulife (MFC) under delivered vs. year ago. Although Telus (T) did better than Bell (BCE) at -9.7%, Telus still lost -5.1%.

The “Bets” portfolio had a return of 3.8%. The travel stocks combined delivered 11.5% growth offset by a steep decline on Boralex (BLX): -21.1%. Unfortunately, the investment in clean energy in 2023 didn’t pay off. I still remain optimistic that we will see a renewed commitment to invest in companies seeking to protect the environment.

2. Plan: Invest in ETF’s that track the major indices as well as in some areas with potential for future growth and that I would like to learn more about.

Result: Investing in ETF’s continue to prove to be a cost efficient way to play in the stock market by buying the indices and also to learn about specific segments. For instance BOTZ (Robotics and Artificial Intelligence) at 30.3% return has been a great way to play in this segment; which has definitely taken off this past year. On the other hand, ICLN (clean energy) and DRIV (autonomous and electric vehicles) provide the opportunity to invest in those segments without committing to one specific company. DRIV was up 16.8% for the year offset by the results of ICLN at -25.4%

3. Plan: Have a split 50/25/25 of equity/GIC/cash with a long term vision of higher equity and lower cash.

Result: Given the faster growth of the stocks in the portfolio, the current split is now 55/22/23 for equity/GIC/cash

Last year's negotiated GIC ladder had 1-year at 5.1%, 2-year at 5.15%, and 5-year at 5.25%.

Following the GIC strategy from an earlier post: “Laddering”, the intent is to renew matured GICs with 5-year GICs, ideally at a higher rate than what it would have been secured a year ago. As the 1-year GIC matured this past week, it was renewed at 5.4% for 5 years.

As for the cash portion of the portfolio, it was invested in the CASH ETF (mentioned in “A Welcome return on Cash”) which currently yields 5.3%. Risk free and 100% liquid! I don’t think we have seen this type of opportunity in at least the past 15 years.

4. Plan: Buy additional stocks if the market hits a predetermined trading range or interest rates are back to historic level.

Result: The stocks bought in 2022 during the market dip were held in the portfolio throughout 2023. No other new stocks were added. Was I too bearish? I prefer to say I was cautious. With the uptick of interest rates, and the escalation of world conflicts, I was glad to have a predetermined trading range so I didn’t need to second guess myself. Besides, as I mention above, the opportunities for risk free returns on cash were hard to pass up this year.

All in all, I’m pleased with the performance of the Stock Talk portfolio this year and look forward to what is coming in 2024.

If you are thinking that 2024 might be the year to start managing your own investments, I would be happy to coach you on how to do the transition to a self-directed platform as well as to help set your investment plan in line with your personal goals and risk tolerance level. On the other hand, if you are already managing your own investments and would like to have someone to support you and exchange ideas with throughout the year, you might want to try the “Financial Coach for a year” program.

If you are curious about how a financial coach could help you, book a free consultation by following the link below so we can discuss objectives and assess how your finances can work harder for you in 2024.

Claudia Soler

December 1, 2023

* Disclaimer: The information contained within this blog is for informational purposes only and it is not intended as a recommendation of the securities highlighted or any particular investment strategy; nor should it be considered a solicitation to buy or sell any security. In addition, this information is not represented or warranted to be accurate, correct, complete or timely. the securities mentioned in this blog may not be suitable for all types of investors and the information contained in this blog does not constitute advice. Before acting on any information in this blog, readers should consider whether such an investment is suitable for their particular circumstances, perform their own due diligence, and if necessary, seek professional advice.